INTRODUCTION

Technology has advanced rapidly over the last few years, eternally modifying how organizations function. As a result of this development, auditors’ approach to audit financial statements was required to alter. Audits used to be undertaken only by groups of accounting professionals manually browsing through massive amounts of financial data. However, given today’s digital world’s digital revolution, it’s crucial that the audit profession evolves its traditional processes and embraces advanced technology tools such as robotics, automation, and cognitive technology. Therefore, it can uncover insights that allow the audit to remain pertinent and efficient, detect fraud and operational business risks, generate financial reports, and adjust their approach to deliver better results. The primary accounting firms have stated that the use of these tools will improve audit reports by simplifying time-consuming projects that are more manual and rote in nature. For example, using artificial intelligence, robotic systems could interact with a client’s systems to instantly transfer and compile data, which was previously done manually by a junior auditor.

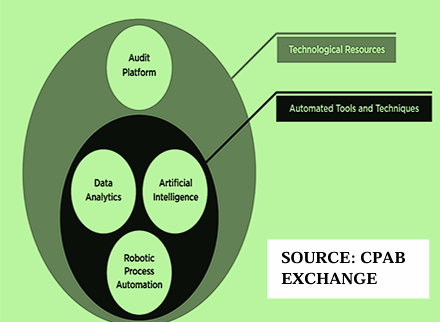

Technology is changing the audit. Audit platforms are becoming more automated. Auditors are increasingly using automated tools and techniques to perform risk assessment and further audit procedures.

– Canadian Public Accountability Board (CPAB)

TECHNOLOGICAL SOFTWARE’S USED IN AUDIT

The auditor should have more time to thoroughly evaluate the more complex and high-risk areas that involves increased auditor evaluation and contain significant amounts of misstatements. According to the sources, such tools will also allow auditors to perform advanced analytics, providing them with increased awareness and gain insight into the firm’s operations. Data analytics may also enable auditors to monitor and analyze their clients’ trends and risks against industry or geographical datasets, allowing them to make more informed decisions and assessments throughout the audit process more effectively. Furthermore, firms claim that with the power of big data, auditors will be able to correlate disparate data information to develop predictive indicators to better identify areas of higher risk, which will lead to better risk identification.

Auditors utilize ATT to undertake risk assessment processes and/or other audit procedures (such as control tests and substantive procedures). Data analytics (DA), artificial intelligence (AI), and robotic process automation (RPA) are examples of ATT.

The following technological resources are employed in auditing:

1. Information technology applications used to manage intellectual resources.

2. Use of IT applications as automated tools and approaches for audit procedures.

Platforms for auditing are getting increasingly automated. Some businesses have built their audit platforms on intellectual resources (such as rules and procedures, ethical standards, auditing warnings and methodology, accounting, industry, and subject-matter guides). Firms are also progressively standardizing their audit operations in order to improve audit uniformity. Automation of audit platforms enables centralized audit monitoring by assurance practice executives at some businesses.

THE PROMISE OF TECHNOLOGY TOWARDS AUDIT

Interpretation of comprehensive data sets

The use of ATT is enabling auditors to examine sizable data sets (often entire populations) to gain deeper insights, spot odd trends, and more forcefully refute claims made by management, which strengthens auditors’ capacity to exercise professional skepticism. That is not to say that auditors test each item in a data set using ATT. The benefit of using ATT is that its output becomes the auditor’s sample of the population rather than a randomly chosen sample that may or may not contain items of audit interest.

Beyond the organizations accounting data

Accounting records of audited entities remain the major source of knowledge for auditors. Although as technology develops, more sources of pertinent data are becoming available, including data from both inside and outside of audited entities. Anticipating that auditors will make use of that data to strengthen the validity of the audit evidence they gather during audits.

Audits performed with enhanced efficiency.

Robots can do repetitive and rule-based jobs significantly more efficiently and accurately than humans. Natural language processing and picture recognition have also improved to the point where they are nearly as accurate as humans. These automated operations make the audit more efficient, but more crucially, when supplemented with a review by the auditor, they may give findings that are as trustworthy as human methods.

Concentrating on high-risk areas rather than basic tasks.

As tedious and repetitive operations can now be automated, auditors may spend more of their time on the audit applying their thoughts to more complicated, subjective aspects of the audit, freeing up auditor time that would previously have been given to the execution of banal duties.

IS TECHNOLOGY TRANSFORMING AUDIT?

It is advantageous to provide some real aspects of ATT that organizations are using to improve audit quality. Auditors have been utilizing ATT for some years to assess the integrity of journal entries. Recently, auditors have been progressively utilizing ATT to do risk assessment and other audit processes (i.e., tests of controls and substantive procedures).

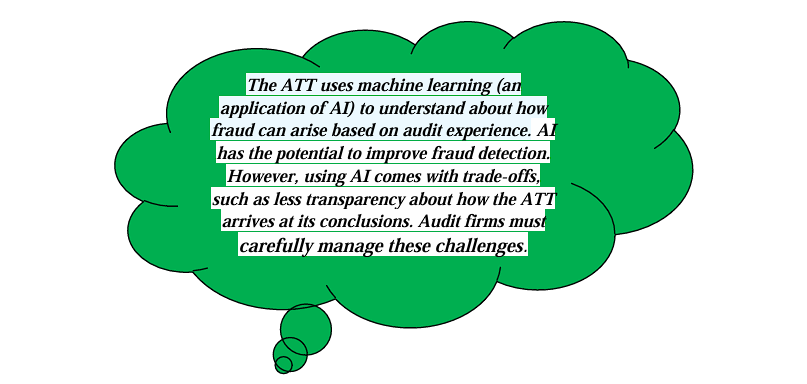

- Evaluating Journal Entries: Financial reporting fraud frequently involves management circumventing internal controls to post fictitious journal entries, for instance. Auditors are increasingly using ATT to classify the population of journal entries in order to detect entries that appear inappropriate or unusual. Auditors determine the filters (and the relative significance allotted to each filter) based on their expectations of how fraudulent The ATT uses machine learning (an application of AI) to understand about how fraud can arise based on audit experience. AI has the potential to improve fraud detection. However, using AI comes with trade-offs, such as less transparency about how the ATT arrives at its conclusions. Audit firms must carefully manage these challenges. 6 | Page entries could arise for the audited entity (e.g., posted by senior management who rarely post journal entries, etc.). Using ATT to identify journal entries of audit interest among thousands of entries is more efficient than visual inspection.

- Assessing the Risks in Auditing: Process mining is an ATT that is being used more frequently in audits. This ATT aids auditors in confirming their comprehension of the flow of transactions for an entity’s cycles (such as sales, purchasing, and payroll), including how they are started in the system and recorded in the general ledger. Process mining can significantly the accuracy of risk evaluations made by auditors. It provides auditors with a more accurate understanding of how the audited entities function

- Substantive Procedures: The three-way match is an illustration of ATT that auditors use to substantively test income. The ATT compares attributes (such as dates, quantities, and prices) from sales transactions that have occurred during the time frame to customer orders, shipping details, and invoices (or invoices, and cash receipts). Exceptions are characteristics that do not meet with supporting accounting records and are examined further by audit firms to evaluate whether they are misleading statements (e.g., revenue recorded prematurely, recorded amounts are inaccurate, etc.). For less complex revenue arrangements where revenue recognition coincides with when goods are shipped to customers, the three-way match routine can be quite effective at detecting errors. However, it does not eliminate the need for auditors to exercise professional skepticism

THE IMPACT OF AUDIT IN THE COMING FUTURE

Given the rapidly growing nature of the technology, research in this area has yielded limited empirical evidence of the benefits of incorporating innovative technology into the audit process. Future research could look at whether incorporating emerging audit technology improves audit effectiveness and efficiency. A quantitative analysis of individual benefits could help improve understanding of the key benefits of using emerging technology in the audit process. In comparison to a quantitative analysis of individual costs, this could help the audit profession decide whether to implement emerging technology.

Technological advances are good or bad for auditing?

Technology has the potential to both enhance the quality of auditing and add value to it. Audit has evolved from a proactive, predictive, forward-looking, real-time effort as opposed to a reactive, backward-looking one. As a result, it offers more chances to assist businesses through timely insights. However, if AI and related technologies are fully used, it may cast doubt on the auditor’s objectivity. “A quality audit necessitates that the auditor always acts independently while carrying out the audit”. At the same time, the familiarity with an audited organization gained from ongoing participation in the engagement improves audit quality.

KEY POINTS TO NOTE

- To keep up with the evolving business model, auditors must modify themselves.

- Among the existing technologies, data analytics is by far the most advanced and is presently used by majority of organizations.

- The adoption of AI in the audit profession has not advanced as far as it could and is still in its initial stages.

- The client-auditor relationship is still crucial because not everything can be replaced with technology.

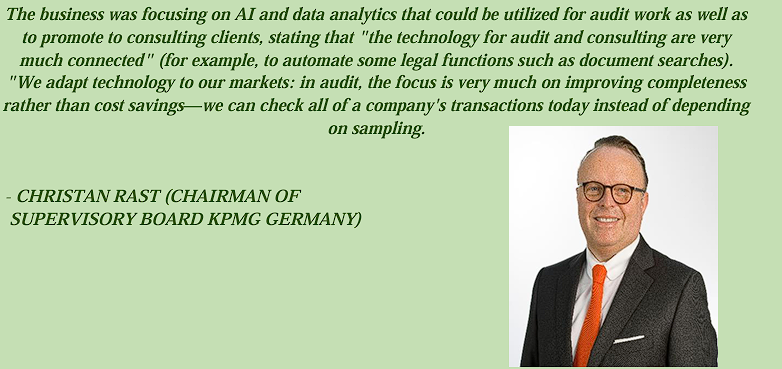

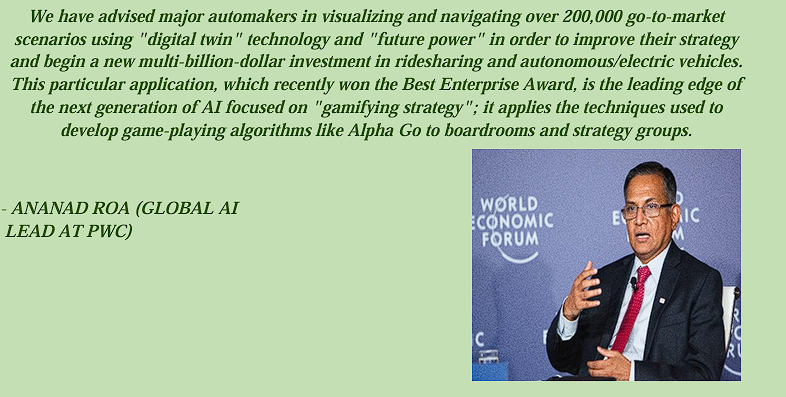

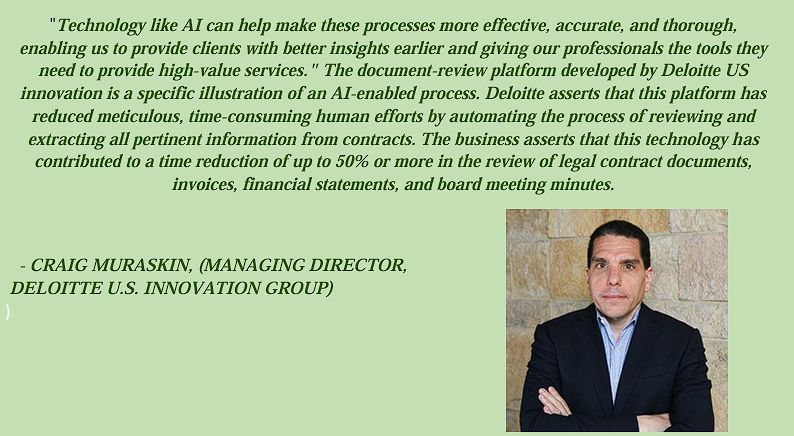

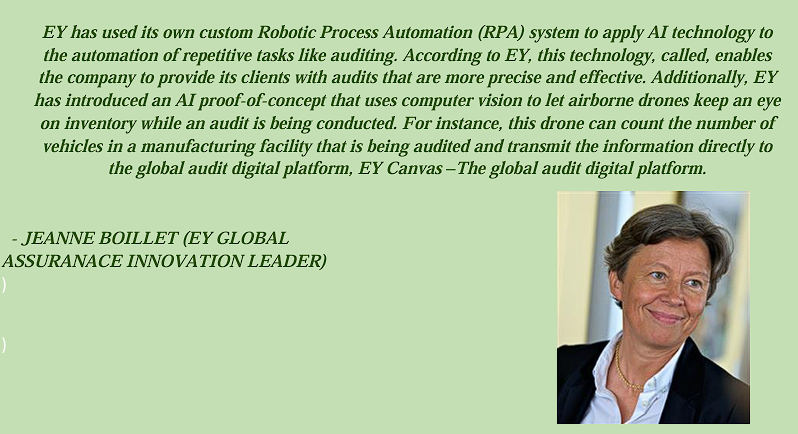

TESTIMONIALS OF TECHNOLOGY’S EFFECT ON MULTINATIONAL CORPORATIONS

Author: Mansi Shah

Assurance & Research Intern